CorpGov: Sell-Side Scarcity Opens Doors for Activists in U.K.

Activist investors are always looking for opportunities and the second Markets in Financial Instruments Directive, colloquially known as Mifid II, may be creating one in the U.K.

The European regulation, which was introduced in 2018, requires banks and brokerages to charge asset managers separately for investment research rather than bundling the fees into the cost of executing trades. Historically research was offered for “free” to entice asset managers.

The legislation was designed to reduce conflicts of interest and inject transparency into the financial industry. However, it has led to a fall in asset managers consuming sell-side analyst research.

A survey by the CFA Institute in early 2019, a year after Mifid II was implemented, found that asset manager research budgets had fallen by 6.3% over the year.

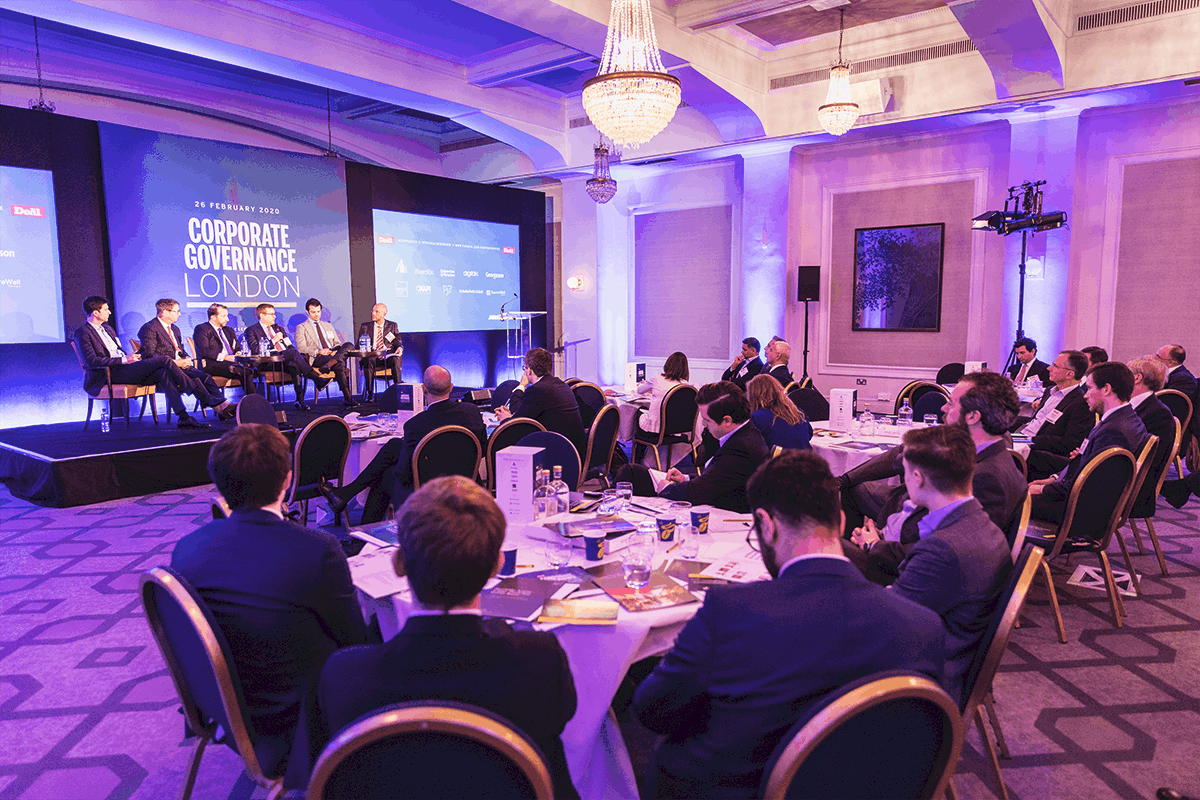

The dramatic cuts in spending on investment research by asset managers in Europe has been a boon to activist investors, panelists at The Deal’s Corporate Governance London conference held on Wednesday, Feb. 26.

Gatemore Capital Management Managing Partner Liad Meidar told delegates that activism in the U.K. is about to enter the “golden age.”

“We are now in the sweet spot with the U.K. somewhere between continental Europe and the U.S. in the terms of its acceptance of activism and yet it is vastly under-penetrated relative to the U.S.,” he said.

That comes as another of other factors are lining up including Brexit, which is creating broader dislocations, and Mifid II.

“Mifid II from our point of view is the single biggest factor that is creating vast opportunities in our space, which is in the small cap area,” Meidar told delegates, adding that it is creating opportunities more broadly as a whole.

He said Mifid II has “fundamentally changed the game of investing and people don’t talk about as much as is relevant to investing today.”

He said the regulation is creating a double-edged sword.

“You have many companies that will issue a profit warning and there will a dramatic over-reaction and largely because people don’t understand what is going on because the companies are undercovered,” he said.

Small cap companies tend to be covered by small brokerage firms, Meidar said, adding that the quality of research tends to be lower.

Indeed, research from early on in the Mifid II process from Brunswick Group LLP showed a 3% drop in the average number of analysts covering FTSE 250 stocks in the first six months after implementation.

Small- and mid-cap companies have seen research coverage fall to an average of 0.6 analysts, and roughly 200 companies have no coverage at all, making it increasingly difficult for companies to reach investors, according to that research.

“So you take a small cap company that used to be covered by four or five houses, now it is covered by two,” Meidar told delegates on Wednesday, “and those two are probably behind paywalls so very few people are reading them.”

This results in “dramatic overreaction” to bad news, but on the flipside when good news is there is hard to get it out, he said.

“Now as an activist a bigger part of our roles is to actually help the company get the good news out too,” he said.

Snow Park Capital Partners Managing Partner Jeffrey Pierce did not mince words calling the regulation a “straight up disaster.”

Rather than giving more transparency, it “just destroyed the markets,” he said.

“But we like to invest in inefficient situations, and it has increased inefficiency,” Pierce said.

As negotiations between the European Union and the U.K. begin on their future relationship, some may be hoping that Mifid II is one regulation that gets scrapped.

“Interestingly,” Meidar said, “the U.K. regulators were one of the driving forces behind Mifid II, so it may be around for quite some time after Brexit.”

Editor’s note: The original version of this article was published earlier on The Deal’s premium subscription website. For access, log in to TheDeal.com.

More From Activism

Activist Investing Today: Glass Lewis' Timmer on AI, Future of Governance

Activist Investing Today: A&M's Peabody, Frankl on M&A Activism Trends

Activist Investing Today: Goodwin's Wood Talks REITs, Biotech Activism